Medicare Supplement Plan vs. Medicare Advantage Plan: What’s The Difference?

There are different ways that you can receive your Medicare coverage, or add onto that coverage. Medicare Advantage and Medicare Supplement insurance are options that may sound similar, but they’re quite different. They do have one main thing in common: they’re both offered by private insurance companies.

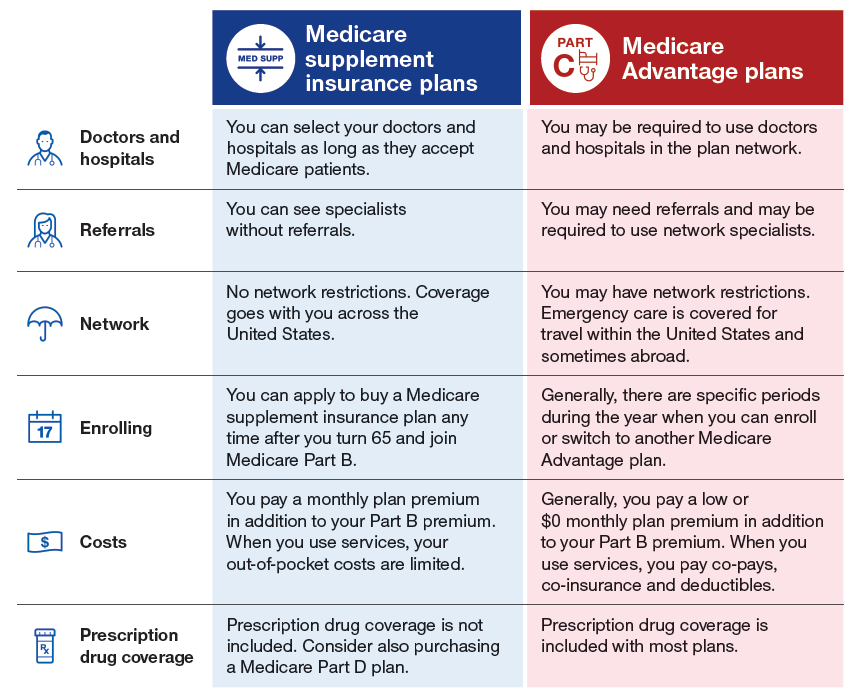

There are two options commonly used to replace or supplement Original Medicare. One option, called Medicare Advantage plans, are an alternative way to get Original Medicare. The other option, Medicare Supplement (or Medigap) insurance plans work alongside your Original Medicare coverage. These plans have significant differences when it comes to costs, benefits, and how they work. It’s important to understand these differences as you review your Medicare coverage options.

Original Medicare, Part A and Part B, is a government health insurance program for those who qualify by age or disability. Part A is hospital insurance, and Part B is medical insurance. There are some out-of-pocket costs associated with Original Medicare, such as copayments, coinsurance, and deductibles. To help with those costs, if you’re enrolled in Original Medicare, you can purchase a Medicare Supplement (Medigap) insurance plan.

Medicare Advantage plans offer an alternative way to receive your Medicare benefits through a private, Medicare-approved insurance company. They must include all your Medicare Part A and Part B coverage (except hospice care, which is covered under Medicare Part A), but may offer additional benefits not included in Original Medicare.

You generally cannot enroll in both a Medicare Advantage plan and a Medigap plan at the same time.

Compare Medicare Plans

Medicare Advantage plans

If you have a Medicare Advantage plan, you’re still enrolled in the Medicare program; in fact, you must sign up for Medicare Part A and Part B to be eligible for a Medicare Advantage plan. The Medicare Advantage plan administers your benefits for you. Depending on the plan, Medicare Advantage can offer additional benefits beyond your Part A and Part B benefits, such as routine dental, vision, and hearing services, and even prescription drug coverage.

There are many different types of Medicare Advantage plans, described below:

- Health Maintenance Organizations (HMOs) require you to use health-care providers in a designated plan network and may require referrals from a primary care physician in order to see a specialist.

- Preferred Provider Organizations (PPOs) recommend the use of “preferred” health-care providers in an established network, and these plans are likely to cover more of your medical costs if you stay inside that network. You don’t need a referral to see a specialist.

- Private Fee-for-Service (PFFS) plans determine how much they will pay health-care providers, and how much the beneficiary is responsible to cover out-of-pocket.

- Medical Savings Account (MSA) plans deposit money into a “health-care checking account” that you use to pay for health-care costs before the deductible is met.

- Special Needs Plans (SNP) are tailored health insurance plans designed for beneficiaries with certain health conditions.

Some of the costs associated with Medicare Advantage might include a monthly premium (not counting your Part B premium, which you must continue to pay as well), annual deductible, coinsurance, and copayments.

To be eligible to enroll in a Medicare Advantage plan, you must be enrolled in Original Medicare, reside in the plan’s service area, and (in most cases) not have end-stage renal disease (ESRD).

Compare Medicare Plans

Medicare Supplement insurance plans

Medicare Supplement insurance, also known as Medigap or MedSup, is also sold through private insurance companies, but it is not comprehensive medical coverage. Instead, Medigap functions as supplemental coverage to Original Medicare. Current Medigap plans don’t include prescription drug coverage.

Medigap plans may cover costs like Medicare coinsurance and copayments, deductibles, and emergency medical care while traveling outside of the United States. There are 10 standardized plan types in 47 states, each given a lettered designation (Plan G, for example). Plans of the same letter offer the same benefits regardless of where you purchase your plan. Massachusetts, Minnesota, and Wisconsin offer their own standardized Medigap plans.

The standardized Medigap plans each cover certain Medicare out-of-pocket costs to at least some degree. Every Medigap plan covers up to one year of Medicare Part A coinsurance and hospital costs after Medicare benefits are used up. But, for example, Medigap Plan G plans don’t cover your Medicare Part B deductible, while Medigap Plan C plans do. So, if you’d like to enroll in a Medicare Supplement insurance plan, you might want to compare the Medigap policies carefully.

While benefits are standardized, the costs are not, meaning they could fluctuate depending on the insurance company offering the plan and location. That is, while Medigap Plan G includes the same coverage no matter where you buy it, the premium for this plan can vary. Also, not every standardized lettered plan is offered in every state.

If you decide to sign up for a Medigap policy, a good time to do so is during the Medigap Open Enrollment Period, a six-month period that typically starts the month you turn 65 and have Medicare Part B. If you enroll in a Medigap plan during this period, you can’t be turned down or charged more because of any health conditions. But if you apply for a Medigap plan later on, you may be subject to medical underwriting; your acceptance into a plan isn’t guaranteed.

No matter whether you enroll in a Medigap policy or a Medicare Advantage plan, you must continue paying your Part B premium.