2014 Medicare Supplement Premiums

Many people notice that rates for their Medigap plans seem to increase from year to year. In most cases, inflation is one predictable cause of Medigap premium increases, but in almost every case there is more to the picture than inflation.

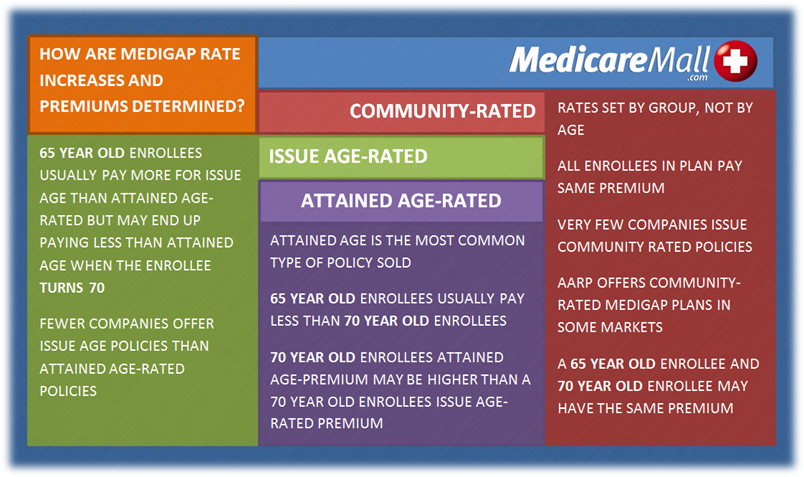

“How is my Medicare supplement premium determined?”

Companies selling Medigap plans can use any of three pricing methods to determine Medigap rates.

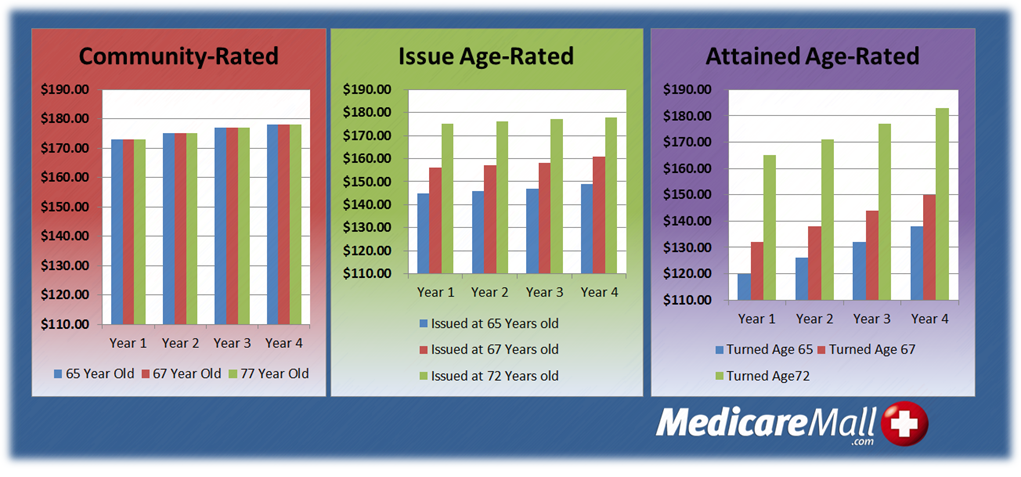

Community-rated policies have no medical underwriting, and age has no bearing on rates. Anyone enrolled in the same Medigap plan within the same zip code area or state pays the same rate as everyone else enrolled in the plan in the same area, regardless of age or medical history. While premiums may increase from year to year, age and health factors have nothing to do with such increases. While community-rated Medigap policies may look attractive to people of more advanced years or people requiring significant medical attention and treatment, policies with community-rated pricing are rare in all parts of the country.

Issue age-rated policies base their rates largely on the age of a person’s first enrollment in the plan. In other words, someone joining a plan at age 65 is going to pay lower rates than someone enrolling in the same plan at age 70. The age when an enrollee joined the plan will continue to play a key role in determining that person’s premium as long as he or she remains enrolled in the plan. While slightly more common than community-rated policies, issue age-rated policies also represent only a small percentage of Medigap policies across the US.

Attained age-rated policies represent the vast majority of Medigap policies. Attained age-rated policies set their premiums according to the policyholder’s current age. In general, Medigap policies setting rates according to current age see more significant increases than community-rated or issue age-rated policies.

“Why does my Medicare supplement premium go up each year?”

The vast majority of Medigap policies are attained age-rated, and priced according to the policyholder’s current age. Because your age can only go up from year to year, your rates are likely to reflect that. While increases vary from company to company, our years of experience indicate that people purchasing attained age-rated policies at age 65 tend to notice the most significant rate hikes between ages 67 and 69.

“How can I lower my Medicare supplement premium?”

Because you are able to apply for a new Medigap policy at any time, it is advisable to compare your current rates to the competition’s from time to time. If you have preexisting conditions, you should be cautious in considering a change, but you have every right to shop the market for new Medicare supplement policies in order to look for lower rates. You may keep the same plan but switch to a company offering a lower rate, or you may decide to switch from one Medigap plan to another. For example, many people looking for the most comprehensive yet affordable coverage choose to upgrade from their current supplement plan to Medigap Plan F.

Comparing Medigap Plans and Quotes might save you money

Finding the lowest Medicare supplement rates available in your area starts with getting a free Medigap quote. Contact MedicareMall for further assistance in ensuring you have the lowest 2014 Medigap premiums.

2014 Medicare Supplement Premiums © 2011-2013 MedicareMall.com